Vietnam’s FDI Outlook for 2016: Trends and Opportunities

By: Dezan Shira & Associates

Editor: Maxfield Brown

Vietnam’s rapid pace of integration into global commerce is likely to yield unparalleled opportunities and record foreign investment in the near to medium term. While speculation on the nature of Vietnamese FDI has been on the rise, the availability of credible data remains scarce.

To help investors make informed decisions about existing opportunities and likely competitors, the following article outlines key findings from some of the first FDI data released by the Vietnamese Ministry of Planning and Investment since the passage of TPP, Implementation of the ASEAN Economic Community, and signing of Vietnam’s FTA with the European Union. Published at the end of January, 2016, this data provides insight on sources, destinations, industries, and vehicles of foreign direct investment. Should any questions arise as a result of this presentation, do not hesitate to contact members of our staff at vietnam@dezshira.com or www.dezshira.com.

Vietnamese FDI: The Outlook in 2016

Initial figures from January’s FDI data show strong year on year growth over 2015. Newly registered projects reached a high of 127, up 186 percent from a year prior. Total FDI from this period was also up over 100 percent – exceeding 1.3 billion dollars. The substantial changes over 2015 help to highlight the increased importance of Vietnam as a destination for foreign capital and underscore the utility of these figures as a means to evaluate the communist nation’s changing reception as an investment destination by potential investors.

For our updated FDI outlook for 2017 click here

Sources of Investment

The Rise of ASEAN

With regard to sourcing, the most notable feature of 2016’s investments lie in the uptake of capital flows originating within ASEAN. Although Vietnam is a choice destination for all within the economic bloc, based on the Vietnamese economy’s low production costs, key investors to watch within the AEC are Malaysia and Singapore – accounting for 18 and 22 percent of Vietnamese FDI respectively.

Party to the TPP and ASEAN simultaneously, companies based in these two countries are able to tap into the combination of Vietnam’s competitive production costs and lowered trade barriers, in conjunction with the predictable government treatment and lucrative tax arrangements found within their respective home markets.

Appetite for investment in Singapore and Malaysia, however, contrast sharply with that of traditional investors within the region such as China, Hong Kong, and Korea – which have seen declines in recent years. Hong Kong – the traditional hub for holding corporations – can be seen to be slowing in relation to Singapore’s more prominent position as a hub for ASEAN investment.

* Based on FDI as of January 2016

RELATED: Dezan Shira & Associates’ Corporate Establishment Services

RELATED: Dezan Shira & Associates’ Corporate Establishment Services

Future Growth: The EU and India

While constituting a small porition of FDI within Vietnam, both India and the EU will likely become increasingly important investors in Vietnam evidenced by strong growth in recent years. Companies based in India have been exponentially increasing investments over the past three years reaching a 4 percent share of FDI as of January 2016 – up 400 percent over last years average. Driving these investment have been increased cooperation on issues of security as well as complimentary production in of goods such as textiles and pharmaceuticals.

The EU, with its recent conclusion of an FTA with Vietnam, is well positioned to tap into Vietnam’s potential. Although current FDI figures likely reflect a wait and see attitude with regard to commitments of capital, the passage of the EU-VN FTA will likely spark an uptake in investment flows. Key investors to watch in this regard include large and profitable economies within the EU such as Germany, as well as Southern producers in Spain and Italy seeking to adjust production to accommodate declines in purchasing power seen since the start of the debt crisis.

Destinations for Investment

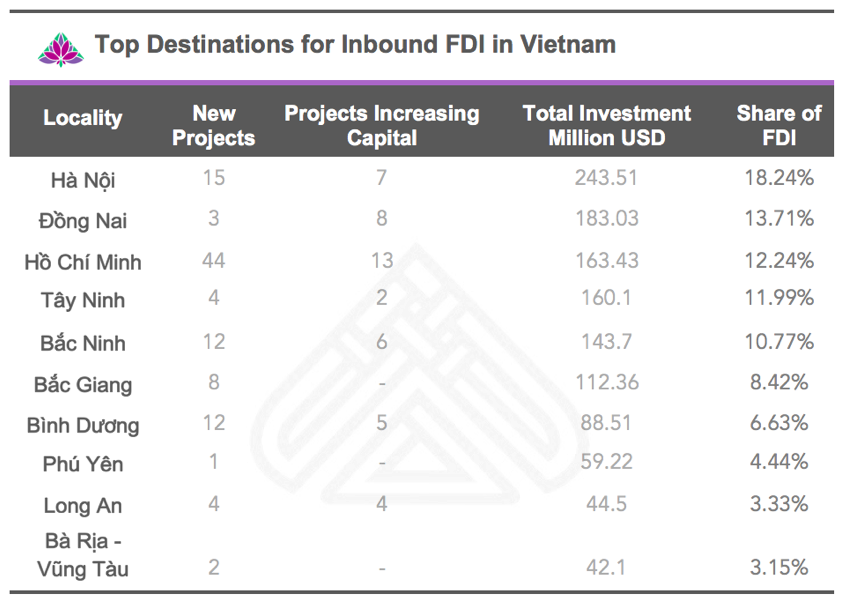

Main Cities

As in previous years, investment continues to be drawn to major cities within Vietnam such as Hanoi and Ho Chi Minh City. Investors within these localities generally benefit from improved access to infrastructure as well as the advantages of agglomeration – stemming from the concentration of talent and resources in areas with more foreign operations.

RELATED: Navigating the Vietnam Supply Chain

RELATED: Navigating the Vietnam Supply Chain

Economic Zones

While Hanoi and Ho Chi Mihn City offer infrastructure and agglomeration advantages, a secondary option for investors lies in Vietnam’s specialized economic zones – of which Industrial Zones (IZs) are the most common. These can be found throughout the country, usually located next to ports, and benefit from tax incentives, improved infrastructure, and streamlined registration procedures. This can help to explain the presence of second tier cities within the top locations for FDI.

Despite the existence of IZs, investments within Vietnam are still heavily focused on three areas: The North, Central, and Southern regions. Even within these three, the north and southern areas of Vietnam receive considerably more investment than their counterpart in central Vietnam. Other locations, while underutilized and lacking in infrastructure, may present opportunities for investors as the Vietnamese government has been activly working to increase incentives in response to a lack of interest.

Investment in Depth

Favored Industries

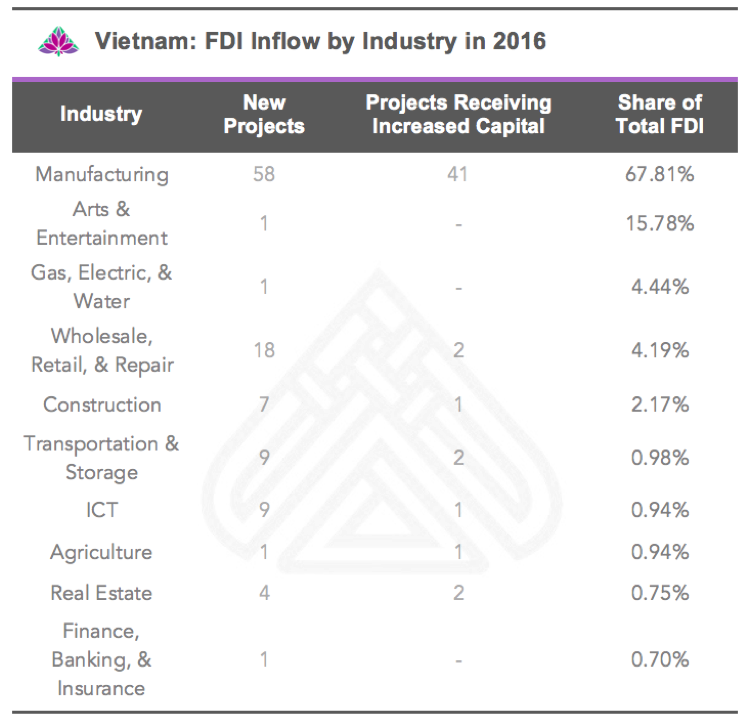

Manufacturing remains a significant attractor of FDI in 2016, accounting for just under 68 percent of all FDI inflows in January. With some of the lowest labor costs in the world, and lowered barriers to trade expected under recent trade agreements, these figures are a confirmation of Vietnam’s competitiveness as a manufacturing hub.

More interesting is the substantial showing for arts and entertainment – which has captured 15 percent of FDI to date in 2016. This is a significant indicator of Vietnam’s growing middle and upper classes – which are projected to number 30 million by 2020. Increasing access to areas such as gambling and shifting opinions on content restrictions for paid media are likely to make the entertainment and related industries volitive but lucrative sectors for investment in the years ahead.

While some industries are currently lagging in investment – such as finance, real estate, natural resources, and ICT – the cause of this is not always a lack of competitiveness. Some industries, such as ICT, show many new projects as firms position themselves to tap into emerging industries such as E-commerce. In these cases, it is likley that capital inflows will take place gradually over the life of a given project.

In other cases, the regulations surrounding a given industry may be inhibiting investment. Although many of Vietnam’s protectionist policies are being dismantled under various FTAs, investments cannot take place without the full implementation of these agreements. Investors should therefore pay close attention to restrictions within Vietnam’s Law on Investment and Law on Enterprises in conjunction with the commitments and implementation timeframes under relevant FTAs.

RELATED: Vietnam’s Product Self-Certification Pilot Scheme Explained

Investment Vehicles

When investing in Vietnam, investors have overwhelmingly chosen to invest via 100% Foreign Owned Enterprises – currently accounting for 80 percent of all Vietnamese FDI projects and just under 75 percent of all capital. Other notable possibilities for investment include Joint ventures and Business cooperation contracts. However, the nature of these investments has proven to be less popular among investors as it requires increased cooperation with Vietnamese counterparts. This being said, and as previously mentioned, certain industries may require foreign investors to invest with the participation of a Vietnamese partner.

It is worth noting that Representative Offices, while a good way to gather information on the Vietnamese market, are not included within these figures in a substantive way. Prohibited from generating profits, ROs are unlikely to register large amounts of capital in Vietnam, and thus little insight on the prospective investors can be gained from assessments of FDI.

Further Support from Dezan Shira & Associates

To learn more about opportunities in Vietnam’s myriad of industrial zones, and to gain insight on how to structure your investments to tap into advantageous incentives, please consult further with the IZ search specialists at vietnam@dezshira.com.

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email vietnam@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight. |

![]()

Investing in Vietnam: Corporate Entities, Governance and VAT

In this issue of Vietnam Briefing Magazine, we provide readers with an understanding of the impact of Vietnam’s new Laws on Enterprises and Investment. We begin by discussing the various forms of corporate entities which foreign investors may establish in Vietnam. We then explain the corporate governance framework under the new Law on Enterprises, before showing you how Vietnam’s VAT invoice system works in practice.

In this issue of Vietnam Briefing Magazine, we provide readers with an understanding of the impact of Vietnam’s new Laws on Enterprises and Investment. We begin by discussing the various forms of corporate entities which foreign investors may establish in Vietnam. We then explain the corporate governance framework under the new Law on Enterprises, before showing you how Vietnam’s VAT invoice system works in practice.

E-Commerce in Vietnam: Trends, Tax Policies & Regulatory Framework

In this issue of Vietnam Briefing Magazine, we provide readers with a complete understanding of Vietnam’s e-commerce industry. We begin by highlighting existing trends in the market, paying special attention to scope for foreign investment. We look at means for online sellers to receive payment in Vietnam, examine the industry’s tax and regulatory framework, and discuss how a foreign retailer can actually establish an online company in Vietnam.

Tax, Accounting, and Audit in Vietnam 2014-2015

Tax, Accounting, and Audit in Vietnam 2014-2015

The first edition of Tax, Accounting, and Audit in Vietnam, published in 2014, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in Vietnam, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in Vietnam.

- Previous Article TPP Insight: Understanding Tariff Reductions

- Next Article Vietnam Regulatory Brief: Nurtition, Special Sales Tax, and Updated Requirements for Representative Offices