Vietnam’s VAT Refund: Expanded Eligibility and Stricter Compliance Rules

Vietnam’s amended Value Added Tax (VAT) Law introduces expanded VAT refund eligibility for investment and export-oriented businesses, while tightening compliance requirements that could expose companies to greater audit scrutiny and refund risks.

Effective July 1, 2025, Vietnam’s revised VAT framework reshapes the country’s refund regime, allowing broader access to refunds for qualifying investment projects, exporters, and businesses subject to the 5 percent VAT rate.

At the same time, the law introduces stricter documentation standards, removes certain refund cases, and reinforces audit oversight.

For manufacturers and foreign-invested enterprises (FIEs), understanding these changes is critical to managing cash flow, securing refund eligibility, and mitigating compliance risks.

See also: Vietnam’s New VAT Law: Key Compliance Guidance

VAT refund under the 2025 VAT Law

According to the new VAT Law enacted in 2025, significant updates have been introduced for VAT refund, in particular:

- Allowing VAT refunds for business expansion investments during the investment stage, where the accumulated input VAT is VND 300 million (US$11,400) or more;

- Businesses with goods and services under a 5 percent VAT rate, if undeducted input VAT reaches VND 300 million or more after 12 months or four quarters, can get a VAT refund. For multiple VAT rates, the refund is based on the revenue ratio; and

- Removing VAT refunds with respect to change of ownership, change of enterprise types, merger, consolidation, separation, and de-merger.

From July 1, 2025, certain cases where the taxpayer applies the VAT deduction method can apply for a VAT refund, including:

- Qualified new projects of taxpayers applying the VAT deduction method that are in the pre-operational investment phase and have accumulated creditable input VAT exceeding VND 300 million;

- Business expansion investments in the investment phase with accumulated creditable input VAT of VND 300 million or more;

- Exporters having excess input VAT creditable over VND 300 million (subject to conditions and the capped refundable amount);

- Certain cases of dissolution, in which businesses using the deduction method can claim a VAT refund if they have overpaid VAT or have input VAT amounts that have not been fully recovered credited;

- Businesses solely producing goods and services with a 5 percent VAT, and with unclaimed input VAT of VND 300 million or more after 12 months or four quarters, can get a VAT refund (For businesses with multiple VAT rates, the refund is based on revenue allocation); and

- Businesses involved in ODA projects or humanitarian aid receiving non-refundable aid can get VAT refunds on goods and services bought in Vietnam for these projects.

Conditions for VAT refund

According to Point 9, Article 15, 2025 VAT Law, businesses should meet these conditions for VAT refund:

- Pay VAT using the deduction method;

- Maintain accounting books and records in compliance with accounting laws;

- Hold bank accounts registered under their TIN;

- Satisfy input VAT deduction rules; and

- Sellers declare and pay VAT on invoices issued to buyers and do not have outstanding tax debt in the requested refund period.

Key highlights where businesses must pay close attention to secure VAT refund eligibility:

- Deferred payment: For goods or services purchased on installment or deferred payment with a value of VND 5 million or more, if there is no non-cash payment documentation at the contractually agreed payment date (including any appendices), the business must declare and adjust the creditable input VAT corresponding to the value of such goods or services in the tax period when the payment is due.

- Imports and subsequently exports: VAT refunds are no longer applicable in cases where the business imports and subsequently exports the same goods. This means that import VAT paid at the time of importation will not be refunded under the VAT refund scheme for export activities.

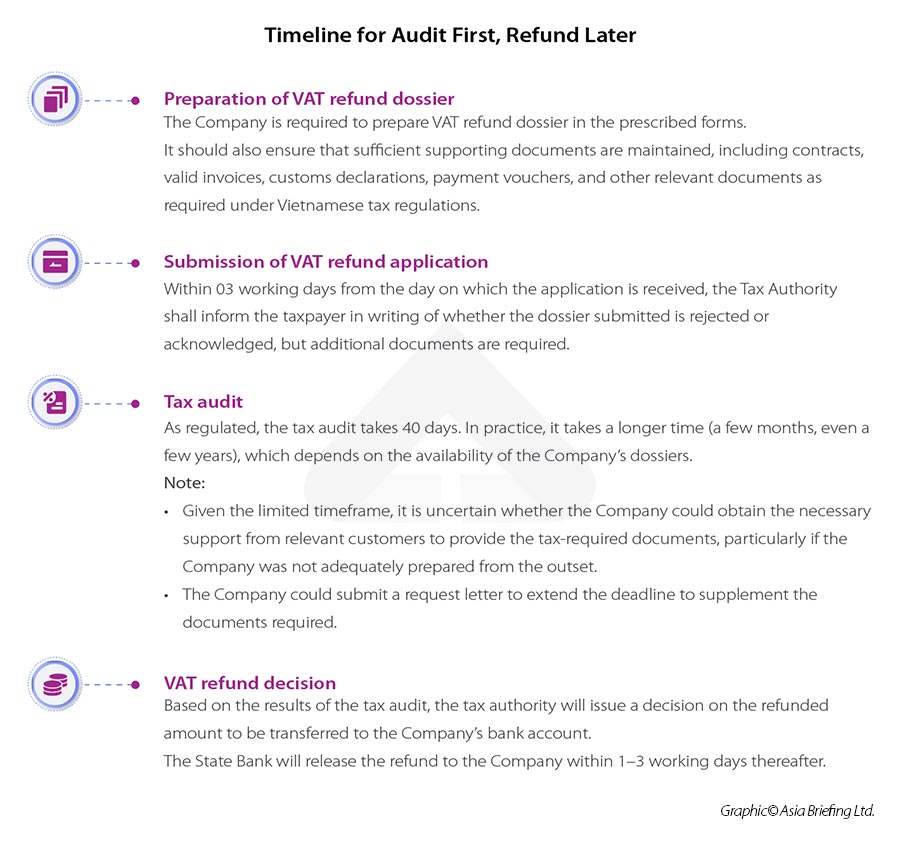

VAT refund process

Tax authorities shall classify VAT refunds and process these claims in accordance with the tax administration, as follows:

- Refund first – audit later: Within a maximum of six working days from the date the tax authority issues a notice of acceptance of the VAT refund dossier, excluding the time required for explanation/supplementation (if any); or

- Audit first – refund later: The timeline for this scheme is summarized below.

Common challenges raised in a tax audit for VAT refund

There are certain cases that could trigger a VAT refund audit, including:

- Input VAT on goods and services not serving business or production activities;

- Declaration and crediting of input VAT based on erroneous invoices recorded in the incorrect tax period;

- Submission of supplementary tax returns after the tax authority has issued conclusions or decisions on tax treatment;

- Declaring input VAT for goods and services serving business and production (Form 01/GTGT) under goods and services for investment projects (Form 02/GTGT), and vice versa;

- Use of invalid invoices or unlawful use of invoices;

- Lack of non-cash payment documents for purchased goods and services required for proper VAT deduction; and

- Exported goods and services without bank payment documents to satisfy conditions for VAT credit and refund.

Case 1: Exported goods sold to a foreign company but delivered within Vietnam

Before July 1, 2025, the application of the 0 percent VAT rate under the on-spot import and export scheme faced aggressive challenges, especially when the foreign buyer had a commercial presence in Vietnam. This position was reinforced by Official Letter No. 1872/BTC-TCT issued by the Ministry of Finance on February 17, 2025. Accordingly, the 0 percent VAT does not apply if a Vietnamese company exports goods to a foreign buyer and either:

- Another Vietnamese company later retrieves the exported goods from the bonded warehouse; or

- The goods are delivered directly to another Vietnamese company.

As of July 1, 2025, new VAT regulations remove the commercial presence requirement and explicitly recognize on-the-spot import and export activities as qualifying for the 0 percent VAT rate. This reform simplifies compliance and provides clarity for transactions involving domestic delivery under foreign buyers’ instructions.

However, for transactions prior to July 1, 2025, where the 0 percent VAT rate has been denied or remains disputed, further clarification and engagement with tax authorities may still be required.

Case 2: Deferred payment under contracts or appendix

According to Official Letter No. 434/VLO-QLDN2 dated August 21, 2025, the Tax Authority confirms that where no non-cash payment document is available by the contractually agreed payment date (including any appendices), the business must declare and adjust the creditable input VAT corresponding to the value of such goods or services in the tax period when the payment becomes due.

This means that for goods or services purchased on an installment or deferred payment basis with a value of VND 5 million (US$190) or more, a non-cash payment is required by the agreed-upon deadline. Otherwise, the corresponding input VAT reduction will be permanently rejected, and any refund claim will be denied.

Takeaway

While the 2025 VAT reform expands refund opportunities, particularly for expansion investments and exporters, it also raises the compliance threshold, making robust documentation, proper invoice management, and timely non-cash payment evidence essential to avoid refund denial or post-refund audits.

See also: Vietnam VAT Rates and Applicability in 2025: A Brief Guide

Managing tax in Vietnam is critical for FDI companies to stay compliant with local regulations, GST requirements, and global standards such as IFRS, navigate complex filings, and apply correct tax treatments. A well-structured tax process helps to avoid penalties and stay 100% compliant.

About Us

Vietnam Briefing is one of five regional publications under the Asia Briefing brand. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Hanoi, Ho Chi Minh City, and Da Nang in Vietnam. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in China, Hong Kong SAR, Indonesia, Singapore, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to Vietnam Briefing’s content products, please click here. For support with establishing a business in Vietnam or for assistance in analyzing and entering markets, please contact the firm at vietnam@dezshira.com or visit us at www.dezshira.com

- Previous Article Decree 29/2026: Vietnam Operationalizes its First Carbon Trading Market

- Next Article