Vietnam’s Payment Preferences: Four Trends to Watch

Vietnam is aiming to move towards a 90 percent cashless economy by 2020 by reducing cash transactions and increasing electronic payments. With 90 percent of current transactions conducted in cash and only 30 percent of citizens having a bank account, the government faces an uphill task to achieve its goals. Nonetheless, recent regulatory reforms and emergence of private players in the last few years have been encouraging towards creating a sustainable digital payments market. In this article, we will look at the current state of the cash based economy, rise of fintech solutions, government cashless policies, rising internet penetration, and what the government needs to do to ensure the transition.

Banking penetration

With only about a third of the 92 million citizens in Vietnam having a bank account, Vietnam offers immense opportunities for growth. In the last seven years, the number of bank accounts has increased from 16.8 million accounts in 2010 to 67.4 million in 2017 according to the State Bank of Vietnam. The government aims to have at least 70 percent of Vietnamese citizens over the age of 15 to have bank accounts by the end of 2020.

In spite of the rise in the number of bank accounts, access to traditional banking services in remote or rural areas remain low and offer an untapped market. Commercial banks and payment service providers need to work together for value addition to their services and focus equally on urban and rural for an inclusive adoption.

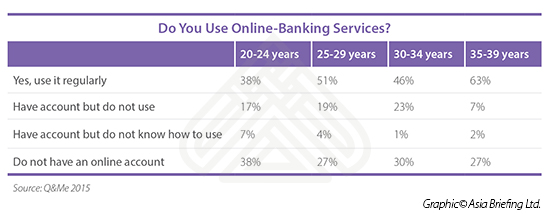

According to a 2015 study, 63 percent of the population above 35 years use online banking, while 38 percent people under 24 years old do not have an online account. Security issue seems to be a major factor for users not opting for online banking solutions. Over 50 percent of users have expressed concerns about security issues in online banking.

Internet and smartphone penetration

According to a recent study by Appota and Google, the internet penetration rate in Vietnam stands at 52 percent. Mobile subscriptions have increased to 131.9 million with the smartphone ownership reaching 72 percent and 53 percent in urban and rural areas respectively. In urban areas, smartphone ownership has almost quadrupled from 20 percent in 2013 to 72 percent in 2016.

The rapid growth of internet usage and smartphone penetration which is driven by cheap smartphones and low service costs will continue to act as enablers and provide the necessary means for digital payment services.

Payment options

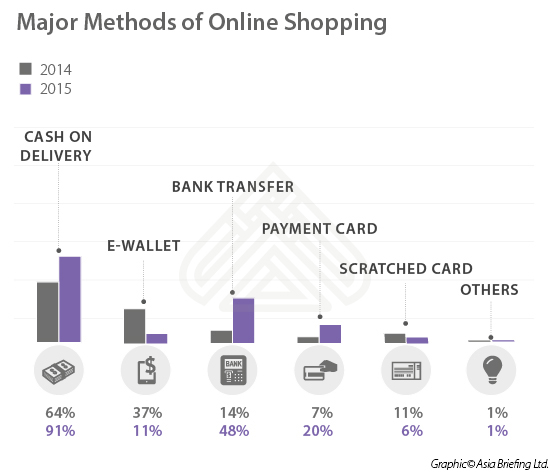

According to the Vietnam E-commerce Report 2015 conducted by the Ministry of Industry and Trade, cash and bank transfers are the most popular forms of payment for buyers. Digital buyers’ use of e-wallets actually declined from 37% to 11% over the same period, while payment cards rose 20 percent. Consumers have little incentive to move away from cash to online banking, digital wallets, or card-based payments due to lack of bank accounts, internet penetration, and a dearth of point-of-sale (POS) terminals.

According to Christian König, a fintech consultant and founder of Finanzpro, which operates several sites on the topic focusing on Europe and Southeast Asia, trust is a major issue amongst Vietnam customers in regards to digital payments. He also highlighted the need for consolidation as there are too many players in the market and increasing cooperation with the commercial banks or global technology firms currently entering the market.

Cash payments

Vietnam has one of the highest cash dominated economy in the world, with almost 90 percent of all transactions conducted in cash. With low banking penetration, lack of ATMs and cashless systems, complexities of digital payment systems, and lack of consumer trust, consumers are compelled to fall back to cash based transactions.

To reduce cash dependence, the government needs to incentivize non-cash systems especially in the e-commerce and bill payment sectors and reduce product complexity for easier adoption. The government also needs to educate the masses to inform about the value proposition of adopting digital payments, as most users do not see any benefits or value in using such a system.

Digital banking

As more and more customers turn to technology for conducting bank transactions, Vietnam offers a huge potential for digital banking. With growing internet access, commercial banks have been developing internet banking services on mobile devices to offer better services. Almost 44 percent of customers of commercial banks have used digital services in 2016 with money transfer/receive, bank cards, and internet banking leading amongst all services.

To promote digital banking, commercial banks in cooperation with digital payment service providers have launched promotions to incentivize digital banking services such as bonus interest rates for deposits and discounts on e-payment of utility bills. Banks should continue to invest in technology in spite of high costs, which will be cost effective in comparison to expanding branch networks. Transactions conducted through digital channels are predicted to contribute 40 percent of banking revenue by 2018.

Payment Cards

Bankcard market in Vietnam has been growing steadily over the years driven by the middle-class, low banking penetration, increase in e-commerce transactions, and new card technologies. Bankcards currently in circulation in Vietnam have increased by 11.36 percent in 2016 to 111 million, in comparison to 2015. However, only 15 percent of users have used the bankcards in 2016. The major reason for low usage is the lack of sufficient ATMs in rural areas, which account for 70 percent of the population. Although the number of point of sales and ATMs has increased by 13.77 percent and 5.39 percent respectively in 2016, banks need to ensure equal distribution of such systems amongst urban and rural areas to increase usage.

On the security front, the government is undertaking numerous measures to increase card security to improve consumer trust. Banks have been instructed to convert magnetic cards into chip cards to increase security and prevent fraud. Authorities also aim to make all ATM cards EMV-standard chip cards by 2020, to reduce risks in e-commerce for both buyers and sellers. Credit card service providers have been instructed to compensate card owners for loss not caused by owners from November 2016 to protect the customer’s interest.

Digital Wallets and Payment Apps

Digital payment solutions or e-wallets offering services such as bill payment, online shopping, and money transfer are fast emerging as alternatives to traditional banking. With a high percentage of internet users and mobile subscribers along with low banking penetration, e-wallets have immense potential in the region. In just one quarter in 2016, e-wallet penetration increased by 50 percent. Currently, almost 10 million customers use e-wallets from over 10 different service providers

To promote e-wallets, the State Bank has released the Circular 39, officially recognizing e-wallet services as a payment service like other payment and collection services. The government has granted licenses to numerous companies in payment services such as 1Pay and WePay, to ensure compliance and security. Commercial banks are also increasing cooperation with e-wallets to further their services and value addition.

Banks such as Vietcombank and Viet Capital Bank have tied up with Payoo app for numerous services. Not only commercial banks but also foreign investment funds and technology firms have stepped up their investments in e-wallet service providers. MoMo, a service of M-Service, which works as an e-wallet and a payment app, has raised a US$28 million Series B round from Standard Chartered Private Equity (SCPE) and global investment bank Goldman Sachs. Similarly, VNPTPay and Payoo received investments from South Korea’s UTC Investment and NTT Data respectively.

Government cashless plans

In light of promoting cashless transactions, the government has launched an ambitious plan to reduce cash transactions in the country to less than 10 percent of total market transactions by 2020. As per the plan, at least 70 percent of water, electronics, and telecommunication service providers will accept cash-free payments from individuals and households. In addition, the plan aims to ensure that at least 50 percent of total urban households use electronic payments for daily transactions by 2020. Along with electronic payments, the government is also focusing on increasing the use of credit cards by ensuring that all supermarkets, shopping malls, and distributors accept credit cards.

The proposal also includes the development of new payment methods for rural areas to increase access to services. By 2020, the government is targeting at least 70 percent of citizens over the age of 15 to have bank accounts to encourage financial inclusion. Government pensions and social welfare systems are also being developed to ensure payment by electronic methods. By 2020, the aim is to reach 200 million transactions a year and having at least 300,000 POS’s installed.

Along with infrastructure development, the government is also focusing on security and safety of such options to ensure consumer protection. In order to reduce risks, the government had issued Circular No.30/2016/TT-NHNN in October 2016, stipulating payment service provision and intermediary payment services, including regulations on security solutions, dealing with claims, ATMs safety as well as legal rights for customers and users of payment services. State Bank of Vietnam has implemented numerous solutions such as accelerating the examination the compliance of legal document on e-payment, card settlements; completing the framework for safety and security of payment system, protecting legal rights and benefits of the customers and providers of payment transactions.

Looking forward

Moving towards a digital economy would require further changes in the regulatory framework and cooperation with the private sector. The government needs to expand banking presence along with ATMs and POS’s in rural areas for inclusive growth. To build consumer trust in online systems and increase adoption, they should incentivize non-cash transactions, simplify digital payment regulations, and ensure a proper grievance redressal system. As digital solutions have to compete with cash, ensuring convenience and security by the use of technology will be instrumental in increasing adoption.

Fintech firms on their part need to diversify services to monetize their customer base by increasing their tie-ups with other services such as utility bill payments, online shopping, money transfer, and others. This will also lead to consolidation, as most users do not prefer to use multiple service providers based on their different requirements.

The move to a digital economy will be a steady process and will require continued government support and private sector investment. This will not only lead to cost savings and increased efficiency for customers and banks but also increase transparency and reduce tax evasion. Foreign investors need to take note of the immense growth potential of digital payments in Vietnam and work with early-stage local startups who understand the market but lack the necessary capital for expansion.

With supportive regulatory changes, implementation of new technologies, increased banking penetration, entry of fintech firms, and growing internet penetration, achieving a 90 percent cashless society by 2020 seems challenging, but achievable.

Vietnam Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices in China, Hong Kong, Indonesia, Singapore, Vietnam, India, and Russia.

Please contact vietnam@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Vietnam Market Watch: Russian Investment, US Trade, and the Rise of Innovation

- Next Article Tax, Accounting, and Audit in Vietnam 2017-2018 – New Publication from Vietnam Briefing