Social Security in Vietnam: Social Insurance

HANOI – When operating their business in Vietnam, foreign companies must ensure that they understand the legal framework which provides for the rights and obligations of employers and employees with respect to social security. There are three types of mandatory social security in Vietnam: social insurance, health insurance and unemployment insurance.

This article will provide an overview of social insurance in Vietnam, highlighting the minimum contributions of both employers and employees, as well as employee benefits including sick leave, maternity leave, allowances for work-related accidents and occupational diseases, pension allowance, and mortality allowance.

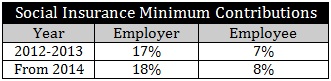

The mandated contributions to the State Social Insurance Fund for 2012 and 2013 are 17 percent of gross income for employers and 7 percent gross income for employees. From 2014, the percentages will be increased to 18 percent for employers and 8 percent for employees.

RELATED: Dezan Shira & Associates’ Payroll and Human Resources Services

RELATED: Dezan Shira & Associates’ Payroll and Human Resources Services

For employees working under an employment contract that is less than three months in duration, the social insurance contribution amount will be included in their salary, and the employees will be responsible for paying their own social insurance or other insurance.

Sick leave allowance

Sick leave allowance is given to employees who are ill, recovering from an accident, or taking care of sick children younger than seven years old. Applicable allowance and leave days vary depending on the number of years the employees have contributed social insurance.

The maximum time granted per year for sick leave is 30 days with less than 15 years of social insurance payment, and can be increased to 60 days where the employees have paid more than 30 years insurance. The allowance granted in lieu of salary is equal to 75 percent of the salary of the previous month.

Certification from a medical care establishment is required to claim sick leave allowance.

Maternity allowance

Employees are entitled to maternity benefits not only when giving birth, but also when adopting children who are less than four months old, provided that they have made social insurance contributions for six months and within twelve months before childbirth or adoption.

On average, female employees have the right to take maternity leave for four months. If giving birth to twins or more, employees are entitled an additional 30 days leave for each extra child.

Female employees who are pregnant are also entitled to take one day leave for each prenatal check-up, with a maximum of five days. Furthermore, they can enjoy maternity benefits for miscarriage, abortion or stillbirth, and even for taking contraceptive measures such as implanting an intrauterine device or sterilization measures.

Maternity allowance each month is equal to 100 percent of the average of salary/wages in the six months preceding the leave. In addition, employees are entitled to a lump-sum allowance equivalent to two months of standard minimum salary for each child upon giving birth or adopting a child of under four months old.

Allowance for work-related accidents and occupational diseases

Employees can enjoy an allowance for work-related accidents or diseases if they suffer from a working capacity decrease of at least 5 percent. Where the decrease is between 5 percent and 30 percent, employees are entitled to a lump-sum allowance. A working capacity decrease of more than 30 percent qualifies them for a pension. A higher allowance is given for a bigger ratio of working capacity loss.

Employees suffering from a working capacity decrease of at least 81 percent will be entitled to an attendance pension equivalent to the standard minimum salary in addition to the pension mentioned above. If an employee dies due to work-related injury or disease, the family shall be paid a lump-sum allowance equivalent to 36 months of standard minimum salary.

Pension allowance

Pension is granted to female employees older than 55 years or male employees older than 60 years with at least 20 years of social insurance contribution. A lower pension will be granted where these aforementioned requirements are not met but other sub-requirements are met.

Monthly pension is calculated upon the number of years of social insurance contribution and the average monthly salary identified for monthly social insurance payment. The maximum pension amount is equivalent to 75 percent of the average salary while the lowest pension is equivalent to the standard minimum salary.

Employees who have made social insurance contributions of more than 30 years for men and 25 years for women are entitled to an old-age grant which is 0.5 percent of the average salary multiplied by the extra years that they contributed. For example, a man retiring after working for 34 years will receive an old age grant of 0.5 percent of average salary multiplied by the extra four years of contribution.

For those ineligible for pension, a lump-sum allowance will be granted depending on years of social insurance contribution. For each year, employees are entitled to one and a half times their average monthly salary.

Mortality allowance

Upon death, whether the employee has been paying into social insurance, deferring payment between jobs, or collecting monthly pension or allowance for a work injury or occupational disease, an allowance equivalent to ten times the standard minimum salary will be paid by the social security fund to cover the funeral.

Upon meeting certain requirements, a survivor allowance equivalent to 50 percent or 70 percent of the standard minimum salary will be given to the family or relatives of employees on a monthly basis, until the relatives cease to meet those requirements or upon their death.

In addition, one-time mortality allowances in varying amounts can also be paid to relatives of deceased persons depending on the case.

Material for this article was taken from Vietnam Briefing’s Doing Business in Vietnam technical guide. This guide aims to assist foreign investors in understanding the business environment of Vietnam, including reasons to invest and challenges for which to prepare. It will help you navigate the legal investment framework and understand the relevant regions for your investment purposes so that your company can take its first steps towards handsome returns. This publication is available as a PDF download on the Asia Briefing Bookstore.

Material for this article was taken from Vietnam Briefing’s Doing Business in Vietnam technical guide. This guide aims to assist foreign investors in understanding the business environment of Vietnam, including reasons to invest and challenges for which to prepare. It will help you navigate the legal investment framework and understand the relevant regions for your investment purposes so that your company can take its first steps towards handsome returns. This publication is available as a PDF download on the Asia Briefing Bookstore.

Dezan Shira & Associates is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in emerging Asia. Since its establishment in 1992, the firm has grown into one of Asia’s most versatile full-service consultancies with operational offices across China, Hong Kong, India, Singapore and Vietnam as well as liaison offices in Italy and the United States.

For further details or to contact the firm, please email vietnam@dezshira.com, visit www.dezshira.com, or download the company brochure.

You can stay up to date with the latest business and investment trends across Vietnam by subscribing to Asia Briefing’s complimentary update service featuring news, commentary, guides, and multimedia resources.

Related Reading

An Introduction to Doing Business in Vietnam

An Introduction to Doing Business in Vietnam

This new 32-page report touches on everything you need to know about doing business in Vietnam, and is now available as a complimentary PDF download on the Asia Briefing Bookstore.

- Previous Article Vietnam to Change PPP Laws

- Next Article Vietnam’s Prime Minister Prioritizes Support for Production and Business