Vietnam’s Tax Outlook in 2016 and Beyond

By Kurt Nguyen

By Kurt Nguyen

Faced with conflicting pressure to upgrade infrasture and boost investment, the Vietnamese government finds itself in a precarious financial position in 2016. The TPP and EVFTA are still a way out, and there is little doubt that adjustment of taxes or spending will likely occur before investment inflows bolster government coffers. From an investment standpoint, the way in which the interim is handled is set to have substantial ramifications for taxation throughout the country and set a precedent regarding future revenue generation.

The State of Vietnamese Finance

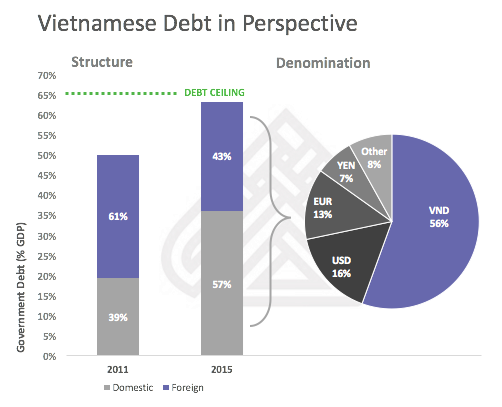

At the core of pressure facing Vietnam is mounting government debt. Despite marginal increases in tax revenue seen in recent months, sovereign debt, which has doubled between 2010 and 2014, is becoming a serious concern. The government’s need for revenue is higher than ever as debt has climbed to 63.3 percent of GDP as of the end of 2015, and is expected to reach 64.5 percent during 2016. In addition to placing a significant burden on authorities in terms of payments and credit constraints, ballooning government spending is dangerously close to reaching the 65 percent debt ceiling imposed by the National Assembly.

Already high on the minds of governing officials, a number of recent events have further curtailed the ability of Vietnam to service its obligations and to make purchases from abroad. Most recently, Brexit has caused the appreciation of the US$ and Yen, placing additional pressure on the government’s foreign denominated debts, 60 percent of which are denominated in US$ or Yen. The appreciation of global safe haven currencies is a small factor, however, in comparison to falling crude oil prices, which have played a significant role in diminishing national foreign exchange revenue. As of 2013, prior to recent commodity price declines, oil accounted for nearly 15 percent of government revenue. While this has declined, government debt has increased as there has been little to replace shortfalls other than deficit spending.

The most immediate solution to the government’s growing debts would be to curtail spending. However, as mentioned above, this is largely tied to infrastructure – a key component in improving Vietnam’s position as an investment destination – and provision of services to Vietnamese citizens – whose rollback would be considered notoriously unpopular. Besides improving the efficiency of its spending, the government is looking to a number of alternatives to increase tax revenue in the medium term. These include focus on economic health and contributions of large corporations, including tax contributions.

While there is a general recognition among authorities that tax incentives as well as FTA-imposed tariff reductions have reduced Vietnam’s tax base, the tool of choice for rectifying shortfalls is agreed to be enforcement of existing laws. By improving the efficiency of tax collection, going after tax evasion, and resolving outstanding tax obligations, it is projected that Vietnam could increase the state revenue by up to 7.5 percent.

Despite the ability of tax hikes to act as a quick fix, the general consensus of analysts so far suggests a government realization that this course of action would be harmful to investor confidence. This is also in line with the World Bank and HSBC’s recommended medium term solution for the growing public debt.

Corporate Income Tax

As part of its ongoing effort to combat tax evasion, the General Department of Tax has set higher goals for tax auditing, resulting in higher frequency of audits and investigations in Hanoi and HCMC. While this has created increased compliance for many companies, only in Hanoi did it increase the tax revenue.

A contributing factor to the failure of audits to directly improve revenue generation is thought to be the announcement of audits in the first place. According to collection trends and litigation data released by the HCMC’s department of tax, scrutiny on domestic SMEs could be responsible for the increased compliance, as auditing-related revenue has fallen in the first six months of 2016 while overall tax revenue has increased.

While domestic SMEs have been the target of investigations in the recent past, calls have also been growing for tax authorities to focus on more visible and lucrative targets such as MNC’s. Many critics point out that SMEs are overburdened by the tax auditing system, which provides an additional layer of compliance over what is already an intensive tax filing process. Vietnam’s tax compliance times are currently Asia-Pacific’s 2nd longest time to file according to the World Bank; this is not including the post-filing procedure of auditing and investigation, which could be lengthened due to the government’s renewed effort.

In the near term, auditing MNCs have been slow to start due to insufficient quantity and quality of tax personnel, who are intimidated by the MNC’s large and capable legal teams. Hence, it is likely that the effects of these polices will be felt more by locals, though large MNC’s may see enforcement ramp up sooner or later.

Personal Income Tax

PIT for salaried workers isn’t directly affected by the increased tax enforcement as it’s collected from the employers. However, PIT for private contractors such as Uber drivers remains a contentious issue. For tax authorities, the loose relationship between employers and contractors make tracking them down very difficult. The possibility of criminal prosecution of such contractors has been mentioned but there has been little movement at present. Enforcement still remains an issue for non-salaried workers; out of 20 million with a tax ID, only 1 million actually paid their taxes.

Some effort has been made to incentivize participation in the tax system by lowering the tax burden. For employees in high-tech sectors, such as IT and high-tech agriculture, they are eligible to receive a 50 percent reduction in PIT. For NGO experts, PIT is now waived on their NGO salary.

RELATED: Understanding Vietnamese Mergers and Acquisitions

RELATED: Understanding Vietnamese Mergers and Acquisitions

Emerging Tax Issues

While increasing enforcement of existing taxes remains a well understood avenue for tax officials to take as they attempt to increase revenue, emerging industries and areas of taxation should also be closely monitored. Even more so than conventional taxation, the manner in which emerging industries are taxed is likely to be of great importance in terms of how Vietnam is viewed as an investment destination for these industries.

The Digital Economy

In the long term, it is likely that new legislation will be drafted to fix the legal loopholes and address challenges that exist within Vietnam’s emerging digital economy. However, authorities are still largely playing things by ear so as to not spook investors. Already, we have seen Vietnam’s first step towards regulating the cyberspace in the enactment of Article 292 of Criminal Code, which requires all e-commerce and online businesses to register and operate under a government license.

However, the Ministry of Justice has promised to consult other departments to tweak the Article in question after concerns from the start-up community has sprung up. In fact, Da Nang, again the pioneer, has promised start-ups a favorable ecosystem despite Article 292. Similarly, the first attempt to tax Uber in its 3 years of operations has been scrapped after getting criticism of its not being comprehensive enough; Uber is now still operating in a legal limbo as the Department of Tax looks into alternatives.

Transfer pricing

In recent months, the Vietnamese government has indicated that it will be stepping up efforts to regulate transfer pricing within the country. For companies with substantial dealing with related entities outside or within Vietnam, this has the potential to increase costs substantially. By the same token, the adoption of more stringent regulation stands to increase tax collections on the part of Vietnam.

In a clear example of increasing enforcement, Vietnam’s tax authority has been going after Thailand’s Central Group and their acquisition of the Big C Vietnam chain from France’s Groupe Casino. It has been almost 3 months since the US$ 1.05 billion transaction was finalized, yet no paper work has been filed and no tax has been paid, which is an estimated US$ 161.4 million, to be paid 10 days after the transaction. Meanwhile, Groupe Casino simply changed the stores’ legal representatives, presumptively to Central Group’s personnel.

The Department of Tax has been looking at existing laws to find the legal basis for extracting the tax, as changing legal representatives is legal. Adding to the list of long-time tax-evading MNCs such as Coca-Cola, Uber, and Formosa, Big C VN case is just another push for GoV towards revision of tax laws. In fact, according to Mr. Dang Ngoc Minh, Deputy of the Department of Tax, the Department has been working with international experts to identify current BEPS (base erosion and profit shifting) risks since 2015. Now, the Department is coordinating with the Ministry of Finance to research current regulations and create a comprehensive BEPS action plan.

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email vietnam@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight. |

![]()

Annual Audit and Compliance in Vietnam 2016

In this issue of Vietnam Briefing, we address pressing changes to audit procedures in 2016, and provide guidance on how to ensure that compliance tasks are completed in an efficient and effective manner. We highlight the continued convergence of VAS with IFRS, discuss the emergence of e-filing, and provide step-by-step instructions on audit and compliance procedures for Foreign Owned Enterprises (FOEs) as well as Representative Offices (ROs).

Navigating the Vietnam Supply Chain

Navigating the Vietnam Supply Chain

In this edition of Vietnam Briefing, we discuss the advantages of the Vietnamese market over its regional competition and highlight where and how to implement successful investment projects. We examine tariff reduction schedules within the ACFTA and TPP, highlight considerations with regard to rules of origin, and outline the benefits of investing in Vietnam’s growing economic zones. Finally, we provide expert insight into the issues surrounding the creation of 100 percent Foreign Owned Enterprise in Vietnam.

Tax, Accounting and Audit in Vietnam 2016 (2nd Edition)

Tax, Accounting and Audit in Vietnam 2016 (2nd Edition)

This edition of Tax, Accounting, and Audit in Vietnam, updated for 2016, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in Vietnam, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who must navigate Vietnam’s complex tax and accounting landscape in order to effectively manage and strategically plan their Vietnam operations.

- Previous Article Puntos clave de la visita del Presidente Barack Obama a Vietnam

- Next Article ¿Por Qué Invertir en la Industria Manufacturera en Vietnam?