Where to Manufacture in Vietnam: Regional Clusters and Location Strategy

Explore Vietnam’s manufacturing location strategy across northern, central, and southern industrial clusters, including infrastructure, labor, utilities, and logistics considerations.

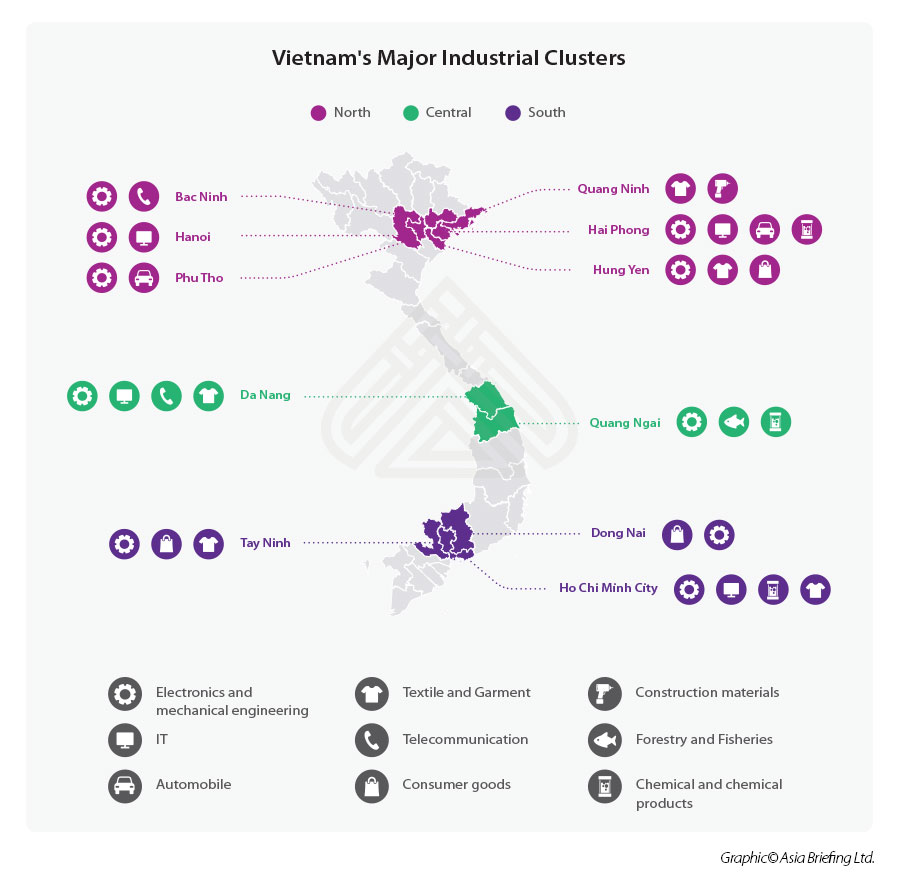

Vietnam’s emergence as a global manufacturing hub relies on three key industrial clusters located in the North, Central, and South. Each cluster features unique cost profiles, logistics networks, and sector strengths that influence investment decisions.

These regional differences in supply chains, labor markets, and industrial focus are vital for foreign investors when choosing sites, estimating costs, and planning long-term growth.

See also: How to Start Manufacturing in Vietnam: A Step-by-Step Guide

Vietnam’s regional manufacturing hubs

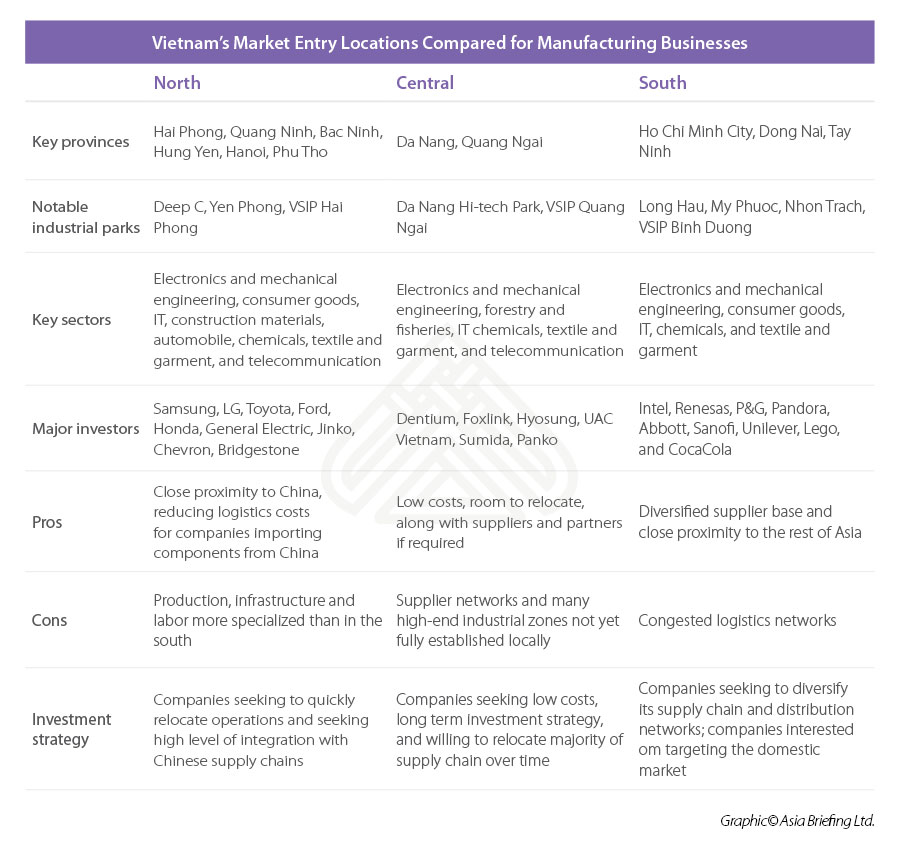

Northern industrial cluster

The northern industrial cluster accounts for approximately 16.2 percent of Vietnam’s total population and is strategically positioned as a key destination for “China plus one” manufacturing strategies. Its geographic proximity to China makes it particularly attractive to time-sensitive production chains that rely on frequent component shipments across borders.

Key features

- Well-positioned for integrated cross-border supply chains with China

- Strong manufacturing base in heavy industries, electronics, mechanical engineering, and textiles and garments

- Mature industrial ecosystems in major provinces and cities such as Hanoi, Hai Phong, and Bac Ninh

- Competitive industrial land supply in core locations, with rising cost pressures in established hubs

Labor force

- Skilled workforce with established expertise in industrial production and export manufacturing

- Concentration of technical and engineering talent supporting electronics and heavy industry supply chains

- Increasing competition for skilled labor in leading industrial provinces

Central industrial cluster

The central region is emerging as a lower-cost alternative to the more saturated northern and southern markets.

While its industrial footprint remains smaller, the region is gaining attention as infrastructure improves and new policy initiatives are introduced.

Key features

- Comparatively lower competition for industrial land and investment projects

- Da Nang, the region’s largest city, benefits from structured urban planning and infrastructure development

- Planned establishment of Vietnam’s first Free Trade Zone in Da Nang

- Attractive as a cost-efficient destination amid rising costs and logistics congestion in the North and South

- Smaller industrial base with limited specialization in advanced manufacturing

Labor force

- Lower labor costs compared to the North and South

- Smaller labor pool relative to the country’s two main industrial centers

- Less intense competition for workers, but a more limited supply of highly specialized manufacturing talent

South industrial cluster

The southern cluster remains Vietnam’s most dynamic and diversified industrial region, attracting the highest number of FDI projects nationwide.

Anchored by Ho Chi Minh City and surrounding provinces, the region combines traditional manufacturing strength with expanding high-tech and innovation-driven sectors.

Key features

- Largest recipient of foreign direct investment projects

- Highly diversified industrial base, spanning traditional manufacturing to advanced industries

- Ho Chi Minh City has developed into a hub for start-ups and technology entrepreneurs

- Strong consumer market presence and established brand identity within Vietnam

- Deep integration into domestic and global supply chains

Labor force

- Large and diverse labor pool supporting a broad range of industries

- Significant reliance on migrant workers from the Mekong Delta and the Central Highlands

- Higher labor costs and turnover rates, particularly in Ho Chi Minh City and Dong Nai

- Intensifying wage pressures in mature industrial zones

Together, these three clusters reflect Vietnam’s increasingly differentiated industrial geography, offering investors multiple entry points depending on sector focus, cost sensitivity, and supply chain strategy.

Identify the Right Manufacturing Location in Vietnam

Choosing between Vietnam’s northern, central, and southern industrial clusters requires balancing labor availability, logistics access, infrastructure readiness, and long-term operating costs. Dezan Shira & Associates’ location analysis and site selection services help investors evaluate industrial zones, compare regional advantages, and identify locations aligned with their manufacturing and supply chain strategy.

Land availability and utilities stability

Land availability

While occupancy rates in Vietnam’s industrial estates are relatively high, typically in the 70-85 percent range, this should not be interpreted as a shortage of available options for new entrants.

Key considerations

- Uneven occupancy across locations and product types: Prime industrial zones near major cities and ports tend to be more saturated, while secondary provinces and newly expanded industrial clusters still offer meaningful land and ready-built factory (RBF) availability.

- Industrial parks developed in phases: Even within estates showing high occupancy, additional land parcels or factory units are often released progressively, allowing investors to enter at different stages.

- Expanding supply: In response to sustained FDI inflows, developers are actively launching new industrial parks and expanding existing ones, with a growing focus on ready-built factories to meet near-term demand and faster setup timelines.

As a result, despite high headline occupancy rates, investors continue to have a broad range of location, scale, and facility options, with further supply expected to come online over the medium term.

Electricity

Vietnam’s industrial electricity supply has remained consistently reliable, with occasional outages mainly during dry seasons due to decreased water levels in hydroelectric reservoirs. To address these issues, the government is actively promoting a transition to renewable energy sources.

According to the Electricity of Vietnam (EVN), Vietnam’s power system ranks second among ASEAN countries in installed capacity. By the end of 2025, the country’s total installed capacity, excluding imported electricity, reached approximately 87,600 MW, a rise of nearly 6,400 MW from 2024.

Power mix

- Renewable energy sources (wind, solar, and biomass) make up about 24,453 MW, or 27.9 percent

- Coal-fired power accounts for nearly 28,100 MW, or 32.1 percent

- Hydropower contributes 24,640 MW, or 28.1 percent

Water and wastewater treatment

Water availability for industrial use in Vietnam remains stable and dependable, as industrial parks are given priority in water supply to support manufacturing and other industrial activities.

According to the Vietnam Water Supply and Sewerage Association, the country’s water infrastructure has advanced significantly over the past 30 years.

Key indicators

- Leakage in water supply has decreased from 17 percent in 2024 to around 15 percent in 2025

- By the end of 2025, there are roughly 1,000 water supply plants with a combined daily capacity of approximately 13.2 million m³

- There are 82 centralized wastewater treatment plants operating with a daily capacity of about 1.79 million m³

Internet infrastructure

Vietnam’s internet infrastructure has rapidly advanced, offering reliable service via fixed broadband, 4G/5G, and fiber-optic connections.

Fixed broadband speeds rose from 173.6 Mbps (33rd globally in March 2025) to 261.8 Mbps (10th globally in August 2025) within five months, placing Vietnam among the fastest broadband markets worldwide. Mobile internet speeds reached approximately 152.2 Mbps in 2025, positioning Vietnam within the global top 20.

Speed and reliability are generally consistent across major cities such as Ho Chi Minh City, Da Nang, and Hanoi, although service costs vary by location and provider.

Vietnam’s seaport infrastructure

As of 2024, Vietnam had 298 seaports with approximately 107 km of wharf length, forming the backbone of the country’s import-export logistics network. International gateway ports in both the north and south allow Vietnam to handle large container vessels and support direct global shipping routes.

Vietnam also operates specialized ports connected to major industrial, petrochemical, and power complexes, capable of handling cargo ships of up to 200,000 tons, liquid cargo vessels of 150,000 tons, and crude oil tankers of 320,000 tons.

Maritime transport dominates Vietnam’s trade flows, with most imports and exports moving by sea and around 40 major international shipping lines operating in the country.

Bottom line

Bottom line

Vietnam’s regional industrial clusters offer distinct advantages for manufacturers depending on their sector focus, supply chain needs, and cost priorities. Investors seeking proximity to China and established export ecosystems may favor the North, while those prioritizing market scale and diversified supply chains may find the South more suitable. Meanwhile, the Central region is emerging as a lower-cost alternative with growing infrastructure and policy support.

A well-planned location strategy can help businesses balance operational efficiency, labor availability, logistics access, and long-term expansion potential in Vietnam.

For international investors, Vietnam's different localities offer favorable conditions across almost every sector, particularly as the country shifts toward higher value-chain manufacturing, high-tech industries, and innovation. Taking a closer look at Vietnam's provinces and investment destinations before committing capital can provide a decisive competitive advantage. A tailored market study, dedicated location selection, or business matchmaking can uncover factors that are often hard to assess—such as special incentives, skilled labor availability, and tax breaks.

About Us

Vietnam Briefing is one of five regional publications under the Asia Briefing brand. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Hanoi, Ho Chi Minh City, and Da Nang in Vietnam. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in China, Hong Kong SAR, Indonesia, Singapore, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to Vietnam Briefing’s content products, please click here. For support with establishing a business in Vietnam or for assistance in analyzing and entering markets, please contact the firm at vietnam@dezshira.com or visit us at www.dezshira.com

- Previous Article Risks Arising From Poor Accounting Documentation Practices in Vietnam

- Next Article