Is Your Business on the List? Vietnam Speeds Up Tax Code Closures for Inactive Firms

In an effort to eliminate the existing backlog within the tax administration, the Tax Department of Vietnam has promulgated Decision No. 595/QD-CT, dated May 8, 2026. This initiative launches a nationwide campaign to accelerate the processing of inactive taxpayer records and unresolved procedures for tax code closure.

Vietnam’s tax authorities have initiated a nationwide campaign to address a long-standing backlog of inactive taxpayer records and unresolved tax code closure procedures. The campaign, launched under Decision No. 595/QD-CT (“Decision 595”), seeks to streamline tax administration, improve the transparency of the business environment, and facilitate the formal exit of dormant enterprises from the market.

The initiative is expected to benefit thousands of enterprises currently classified under tax administration statuses associated with business inactivity, while also strengthening enforcement against taxpayers that fail to comply with tax obligations.

Overall objectives of the 2026 campaign

The campaign forms part of a broader effort to clean and standardize taxpayer data while preventing the misuse of legal entities for tax fraud and other unlawful activities.

The Tax Department aims to:

- Reduce the number of taxpayers classified as inactive but not yet formally dissolved;

- Resolve pending tax code closure applications;

- Improve taxpayer data quality and transparency;

- Prevent the creation of new inactive taxpayer cases;

- Strengthen tax compliance and enforcement; and

- Support compliant businesses and investors by removing administrative bottlenecks.

According to the tax authorities, the campaign is intended not only to enhance tax administration but also to establish a more professional, transparent, and efficient regulatory environment throughout the taxpayer lifecycle, from registration to dissolution, thereby improving the investment climate and attracting both domestic and foreign investment.

Key taxpayer groups under review

The campaign focuses on three primary categories of cases.

Taxpayers under Status 03

Status 03 applies to taxpayers that have ceased operations but have not completed procedures to terminate the validity of their tax identification numbers.

Many businesses in this category stopped operating years ago, but never finalized tax closure procedures. As a result, they remain active within tax administration systems despite no longer conducting business activities.

Taxpayers under Status 06

Status 06 refers to taxpayers that are no longer operating at their registered business addresses.

These cases often arise when businesses relocate without updating registration information or abandon their registered locations entirely. Tax authorities consider this category particularly high-risk because it may be associated with unresolved tax obligations or potential compliance violations.

Individuals whose identities were misused

The campaign will also address cases involving individuals whose personal information was stolen, falsified, or otherwise misused to establish companies, household businesses, or legal entities that do not engage in genuine commercial activities.

Authorities intend to coordinate with relevant agencies to identify and resolve such cases.

Compliance enforcement

The campaign contains stronger enforcement measures, as the Tax Department plans to:

- Review all Status 06 enterprises that issued e-invoices but failed to submit tax declarations;

- Publicly disclose information regarding non-compliant taxpayers where permitted under tax administration regulations;

- Conduct risk assessments and compliance reviews; and

- Refer cases involving potential criminal conduct to law enforcement authorities for investigation.

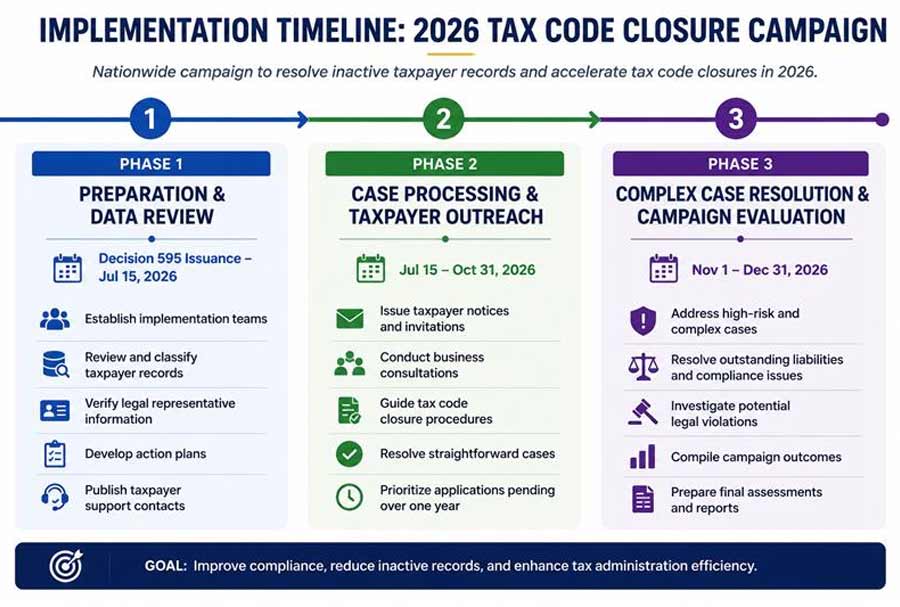

Implementation timeline

The campaign will be carried out in three phases throughout 2026.

Phase 1: Preparation and data review

From the issuance of Decision 595 through July 15, 2026

During this phase, authorities will establish implementation teams, review taxpayer databases, verify legal representative information, classify cases, and create detailed action plans.

Tax offices will also publish contact points for taxpayers seeking assistance.

Phase 2: Implementation and case processing

July 15, 2026, to October 31, 2026

The second phase focuses on taxpayer outreach and case resolution.

Activities include:

- Issuing notices and invitations to taxpayers;

- Conducting meetings with businesses;

- Providing guidance on closure procedures;

- Resolving straightforward cases; and

- Prioritizing applications that have remained pending for more than one year.

Phase 3: Complex case resolution and campaign evaluation

November 1, 2026, to December 31, 2026

The final phase targets more complicated cases involving high compliance risks, unresolved liabilities, or potential legal violations.

Authorities will also compile campaign results and prepare final assessments.

What businesses should do

For companies that have already submitted tax code closure applications but have not yet received final approval, or whose tax audits remain pending, the campaign may present an opportunity to expedite processing.

Given the Government’s target of resolving at least 35 percent of eligible pending Status 03 cases by the end of 2026, businesses with longstanding applications may wish to proactively contact their local tax authorities to verify the status of their applications and determine whether additional documentation is required.

Businesses that have not yet initiated tax code closure procedures should consider preparing relevant records in advance. Depending on the company’s circumstances, tax authorities may require documentation such as:

- Enterprise registration certificates;

- Corporate seals;

- Digital signature token for tax filing

- Tax filing credentials;

- Accounting records and supporting documentation;

- Invoices and transaction records;

- Bank statements;

- Tax declarations; and

- Other supporting documents related to business operations.

Companies should also review and ensure that all outstanding tax returns are filed, and that any outstanding tax liabilities and penalties are reconciled and settled, from the date of establishment up to the date of dissolution, before commencing dissolution procedures.

For enterprises with no revenue, no significant expenses, and minimal historical activity, the closure process may be significantly simpler, typically involving the completion of outstanding declarations and settlement of any remaining license tax obligations.

Need assistance with business dissolution or tax compliance in Vietnam?

Dezan Shira & Associates’ Business Advisory Services can help companies navigate tax code closure procedures, tax audits, deregistration requirements, and corporate compliance matters throughout the business lifecycle. Contact our advisors to discuss your specific situation and ensure a smooth closure process.

Outlook

Decision 595 represents one of Vietnam’s most comprehensive efforts to address inactive taxpayer records and unresolved tax code closure procedures. By combining administrative reform, taxpayer support, data-cleansing initiatives, and enforcement measures, the government aims to reduce long-standing inefficiencies and improve the integrity of the country’s tax administration system.

For businesses that have suspended operations without completing tax closure procedures, the campaign offers both an opportunity and a warning: authorities are expected to accelerate the resolution of legitimate applications while simultaneously increasing scrutiny of taxpayers that fail to comply with legal obligations.

Managing tax in Vietnam is critical for FDI companies to stay compliant with local regulations, GST requirements, and global standards such as IFRS, navigate complex filings, and apply correct tax treatments. A well-structured tax process helps to avoid penalties and stay 100% compliant.

About Us

Vietnam Briefing is one of five regional publications under the Asia Briefing brand. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Hanoi, Ho Chi Minh City, and Da Nang in Vietnam. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in China, Hong Kong SAR, Indonesia, Singapore, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to Vietnam Briefing’s content products, please click here. For support with establishing a business in Vietnam or for assistance in analyzing and entering markets, please contact the firm at vietnam@dezshira.com or visit us at www.dezshira.com

- Previous Article Vietnam’s New Customs Penalty Decree: Key Compliance Changes for Importers and Exporters

- Next Article